Assets vs Liabilities: The Money Equation Your School Never Taught You (And Why You're Probably Confusing the Two)

By: Compiled from various sources | Published on Jan 28,2026

Category Beginner

Description: Understand assets vs liabilities with clear examples. Learn what truly builds wealth versus what drains it, and why your car probably isn't the asset you think it is.

Let me tell you about the moment I realized I'd been financially illiterate my entire adult life despite having a college degree and a decent job.

I was talking to a financially successful friend about my "assets." I listed my car (nice sedan, only two years old), my furniture (good quality stuff), my electronics (latest phone, laptop, TV), my designer clothes. I felt pretty good about my "assets."

He looked at me and said: "Those aren't assets. Those are liabilities pretending to be assets. They're costing you money every month and losing value. An asset puts money in your pocket. A liability takes money out. Which are yours doing?"

I stared at him. My car cost me monthly payments, insurance, gas, and maintenance while depreciating 20% per year. My furniture was worth maybe 10% of what I paid. My electronics were outdated within months. My clothes... let's not even discuss resale value.

I had zero actual assets and thousands of dollars in liabilities that I'd been proudly calling assets because I owned them.

Assets vs liabilities explained is the fundamental financial concept that determines whether you build wealth or perpetually struggle despite earning decent income. Understanding the difference—actually understanding it, not just nodding along—changes everything about how you make financial decisions.

What is an asset and what is a liability sounds obvious until you realize most people (including past me) misclassify things constantly. They think ownership equals asset. They think "I paid a lot for it" means asset. They think "It's nice/useful" means asset. None of that is correct.

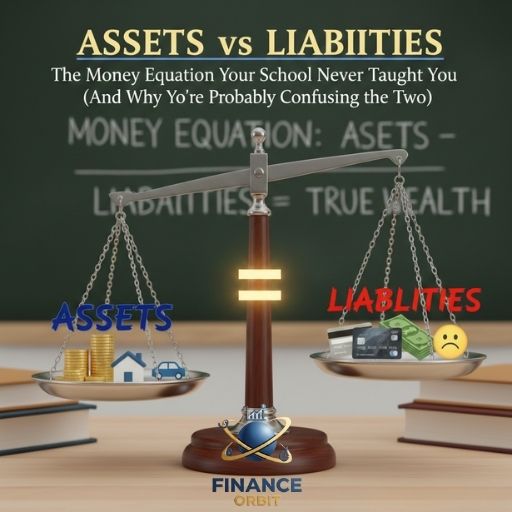

The simple definition that changed how I think about money: Assets put money in your pocket. Liabilities take money out. That's it. Not value. Not ownership. Not usefulness. Cash flow direction determines classification.

So let me walk through assets and liabilities with examples that shatter common misconceptions, explain why people stay broke while earning good money, and show exactly what real wealth building looks like versus the illusion of wealth.

Because your financial education failed you. School taught you algebra but not cash flow. You learned history but not how money actually works.

Time to fix that.

The Simple Definition That Changes Everything

The clearest, most actionable way to understand assets versus liabilities comes from Robert Kiyosaki's Rich Dad Poor Dad, which despite being somewhat controversial in other claims, nailed this distinction perfectly.

Assets put money IN your pocket. They generate cash flow. They produce income. They increase your wealth over time. When you own an asset, money flows TO you.

Liabilities take money OUT of your pocket. They cost you money to maintain. They require cash outflow. They decrease your wealth over time. When you own a liability, money flows AWAY from you.

That's it. Cash flow direction determines classification, not purchase price, not perceived value, not ownership, not usefulness. This simple rule exposes the truth about most things people think are assets.

Your house might be an asset. Or it might be a liability. Depends entirely on whether it generates income or costs you money monthly. Your car is almost certainly a liability unless it's generating income somehow. Your education could be an asset if it increased your earning power more than it cost. Or it could be a liability if you're paying student loans for a degree that didn't improve your income.

Why this matters: Rich people accumulate assets. Poor and middle-class people accumulate liabilities while thinking they're assets. The difference determines who builds wealth and who works forever while staying broke.

Your Car: Almost Definitely a Liability (Sorry)

Let's start with the biggest misconception: your car is an asset because you own it and it has value.

Your car is a liability for the overwhelming majority of people. Here's the math that proves it.

Monthly costs: Car payment (if financed), insurance, gas, maintenance, repairs, registration fees, parking, tolls. Let's say conservatively $500-800/month total for a typical car. That's $6,000-9,600 annually leaving your pocket.

Depreciation: New cars lose 20-30% of value in the first year, 15-20% each subsequent year for the first five years. A $30,000 car is worth maybe $24,000 after one year, $20,000 after two years, $16,000 after three years. You're losing thousands in value annually.

Cash flow direction: Money flows OUT of your pocket consistently. Insurance bill—out. Gas—out. Maintenance—out. The car gives you nothing back financially. It provides transportation utility, but utility isn't cash flow.

When a car becomes an asset: If you use it for Uber/Lyft and the income exceeds all costs (rare). If you rent it out on Turo and profit exceeds costs. If it's a classic car that appreciates in value while also generating rental income or appreciation gains. For 95% of people, none of these apply.

The mental trap: People think "I own it, therefore it's an asset" or "It's worth $20,000, therefore I have a $20,000 asset." Wrong. It's a depreciating liability that costs you thousands annually while its resale value plummets. The only accurate way to classify it: liability.

The better approach: If you must have a car, buy reliable used cars with cash, minimize the liability. Better yet: live without a car if possible (urban areas with public transit), or buy the minimum vehicle that meets needs, not wants.

Your Primary Residence: Asset or Liability? (It's Complicated)

This is controversial because culturally we're taught "home ownership builds wealth" and "rent is throwing money away." Sometimes that's true. Often it's not.

Your house is a liability if you live in it and pay mortgage, property taxes, insurance, maintenance, HOA fees, and utilities—all while it generates zero income. Money flows OUT every month. Yes, you're building equity through mortgage payments (the portion going to principal, not interest), but the total cash outflow typically exceeds equity building for years.

Monthly costs of homeownership: Mortgage payment (if not paid off), property taxes, homeowners insurance, HOA fees (if applicable), maintenance (budget 1-2% of home value annually), utilities, repairs, renovations. For a $300,000 home with a mortgage, you might spend $2,000-3,000+ monthly. That's $24,000-36,000+ annually leaving your pocket.

Opportunity cost: The down payment (say $60,000) could have been invested elsewhere generating returns. Instead it's locked in home equity generating zero cash flow.

Appreciation is uncertain: Home values sometimes increase, sometimes decrease, sometimes stagnate. The 2008 financial crisis reminded millions of homeowners that appreciation isn't guaranteed. And even if your home appreciates, you can't access that value without selling or borrowing against equity (creating more liability).

Your house becomes an asset if you rent out rooms (income exceeds your costs), rent the entire property (rental income exceeds mortgage and expenses), or it appreciates significantly and you sell for profit. But while you're living in it paying costs, it's functionally a liability regardless of equity building.

The accounting perspective: Traditional accounting classifies your home as an asset because it has value. But from a cash flow perspective—the one that matters for wealth building—it's a liability if money flows out monthly.

Why people defend this: Home ownership has psychological and lifestyle benefits—stability, freedom to modify, pride of ownership, forced savings through equity building. These are real but separate from the asset/liability cash flow question. You can acknowledge your home is a liability while still valuing it for other reasons.

The better approach: If buying a home, calculate total cost of ownership honestly (not just mortgage payment). Consider renting rooms or portions to generate income. Or consider house hacking (buying multi-unit property, living in one unit, renting others). Only then does your residence potentially become an asset.

True Assets: Things That Actually Put Money in Your Pocket

Now let's cover what real assets look like—things that generate income or appreciate while costing minimal or nothing to maintain.

Rental Real Estate (Done Right)

Investment property that generates rental income exceeding all costs (mortgage, taxes, insurance, maintenance, vacancy reserves, property management) is a true asset. Every month, money flows INTO your pocket.

Example: You buy a duplex for $300,000, live in one unit, rent the other for $1,500/month. Your mortgage/taxes/insurance total $2,200/month. The rental income covers $1,500 of that, leaving you paying $700/month to live somewhere while building equity. Eventually you move out, rent both units for $3,000 total, while costs stay $2,200—now you're cash flowing $800/month. That's an asset.

The challenge: Requires significant capital, carries risk (vacancies, bad tenants, repairs), demands time or management fees. It's not passive income initially. But done correctly, rental real estate is one of the most proven wealth-building assets.

Dividend-Paying Stocks and Index Funds

Stocks that pay dividends generate cash flow. You own shares, companies pay quarterly dividends, money arrives in your account. The stock value might fluctuate, but the dividends provide actual income.

Example: You invest $10,000 in a dividend ETF yielding 3% annually. You receive $300/year in dividends regardless of stock price fluctuations. Reinvest those dividends and they compound over time. This is an asset generating cash flow.

Index funds that appreciate are slightly different—they don't generate cash flow until sold, but they reliably grow in value (historically 7-10% annually over long periods). Some would classify these as assets because they're building wealth even without immediate cash flow. Others are stricter and say no cash flow = not technically an asset yet. Either way, they're infinitely better than liabilities.

Bonds and Fixed-Income Investments

Bonds pay interest on a schedule. You lend money (to government or corporation), receive regular interest payments, get principal back at maturity. This is predictable cash flow—a true asset.

Example: $10,000 in treasury bonds yielding 4% pays $400 annually. Not exciting returns, but it's actual money flowing to you.

Business Ownership (Profitable Businesses)

Owning a business that generates profit beyond what you must reinvest makes it an asset. Whether you actively run it or own passively (like silent partner), if money flows to you, it's an asset.

Example: You own 30% of a profitable local restaurant. It distributes $2,000 monthly to owners based on profits. That $600/month flowing to you makes your ownership stake an asset.

Your own business counts if it generates income exceeding the time/money you put in. If you work 80 hours weekly for minimal profit, it's arguably more liability than asset (costing you opportunity cost of earning elsewhere). If it generates significant profit for reasonable time investment, it's an asset.

Intellectual Property That Generates Royalties

Books, music, patents, courses, or other IP that generates ongoing royalties is an asset. You create once, earn repeatedly.

Example: A book generating $500/month in royalties years after publication. A patent licensed to companies generating royalty payments. An online course selling passively generating income. These are assets—money flows to you without ongoing equivalent effort.

High-Interest Savings or CDs

Money in high-yield savings accounts generates interest. Not much (maybe 4-5% currently), but it's cash flow. Your money makes money.

Example: $50,000 in a high-yield savings account at 4% generates $2,000 annually in interest. That's cash flowing to you, making it an asset (albeit a low-return one).

The distinction: Regular checking account earning 0.01% interest essentially generates zero cash flow—functionally not an asset. High-yield accounts generating meaningful interest qualify.

Common "Assets" That Are Actually Liabilities

Let's expose the items people mistakenly classify as assets when they're definitively liabilities.

Your Wardrobe and Designer Goods

Designer clothes, handbags, shoes cost money to buy and generate zero income. They depreciate immediately—used designer goods resell for fraction of purchase price. Storage costs money (closet space, cleaning, organization). They don't appreciate (except rare collectibles). Cash flows OUT, never IN.

The mental trap: "But it's a Chanel bag worth $5,000!" So what? Does it generate income? Does it appreciate? Will you sell it for more than you paid? No, no, and definitely no. It's a liability you enjoyed purchasing, but it's still a liability.

Electronics and Gadgets

Your phone, laptop, TV, gaming system—all cost money to purchase, depreciate rapidly (electronics lose value faster than almost anything), cost money to maintain/upgrade/repair, and generate zero income unless you're using them for income-generating work.

Example: $1,200 iPhone depreciates to $600 value within a year. You pay monthly for service ($80/month = $960/year). Total cost: $1,560 in first year. Income generated: $0 (unless it's a business tool generating more than it costs). That's a liability.

Furniture and Home Decor

Furniture loses 70-90% of value immediately. A $3,000 couch resells for $300-500 if you're lucky. It generates no income. It costs money to move, clean, and eventually replace. Liability.

Collectibles are sometimes claimed as assets ("It'll appreciate!"). Most don't. Even if they do, they generate zero cash flow until sold, and carrying costs (storage, insurance) make them liabilities until that hypothetical future sale.

Boats, RVs, Motorcycles, Jet Skis

The saying "a boat is a hole in the water you pour money into" exists for good reason. Purchase price, insurance, registration, maintenance, storage, fuel—all substantial costs. Income generated: zero (unless you charter it commercially, which almost nobody does).

These are lifestyle choices, not investments. Buy them if you want and can afford them, but understand clearly: they're liabilities. Expensive liabilities.

Gym Memberships and Subscriptions

Monthly subscriptions are liabilities—money flows out regularly. They provide value (entertainment, convenience, fitness), but value isn't the same as financial return. Netflix is a liability. Gym membership is a liability. They're worthwhile liabilities perhaps, but still liabilities.

Your Education (Sometimes)

Student loans for a degree that doesn't increase earning power is a liability. If you paid $100,000 for a degree and now earn $35,000 annually when you could've earned $32,000 without the degree, you've got a massive liability providing minimal return.

The degree becomes an asset only if increased earning power exceeds the cost over your career. Medical degree costing $300,000 but increasing lifetime earnings by millions? That's arguably an asset (or at least a positive-ROI liability that transitions to asset status).

The Cash Flow Test: How to Classify Anything

When unsure whether something is an asset or liability, apply the cash flow test with these questions.

Does it generate income? If yes, how much? If no, it's likely a liability. Income generation is the primary asset indicator.

Does it cost money to maintain? If yes, how much? Compare maintenance costs to any income generated. If costs exceed income, it's a liability regardless of perceived value.

Is it appreciating or depreciating? Appreciation alone doesn't make something an asset (it generates no cash flow until sold), but depreciation confirms it's a liability.

Could I rent it out or monetize it? If you could but aren't, it's a liability. If you are monetizing it and profiting, it's an asset.

If I lost my job tomorrow, would this help or hurt my financial position? Assets would continue generating income. Liabilities would continue draining resources.

What would happen if I sold it? Would you recoup your investment? Make a profit? Take a massive loss? This reveals true value versus purchase price.

Example application—evaluating a car:

- Does it generate income? No (assuming personal use).

- Does it cost money to maintain? Yes ($500+/month).

- Is it appreciating or depreciating? Depreciating rapidly.

- Could I monetize it? Possibly (Uber/Turo), but I'm not.

- If I lost my job, would this help or hurt? Hurt—ongoing costs without income.

- If I sold it, would I recoup investment? No—already lost 20% to depreciation.

Conclusion: Liability. The cash flow test confirms it definitively.

Why People Stay Broke: The Asset/Liability Confusion

Understanding why people earn good money but never build wealth becomes clear through the asset/liability lens.

The typical middle-class pattern: Get a job, earn decent income, immediately increase spending to match income (lifestyle inflation). Buy a car (liability), buy or rent a house (liability if owner-occupied), furnish it (liability), fill it with electronics (liability), buy nice clothes (liability), finance a lifestyle (all liabilities).

Result: High income, high expenses, zero or negative cash flow, no wealth building. You own lots of stuff but possess no assets. You look successful but are functionally broke—one job loss away from financial crisis.

The wealth-building pattern: Get a job, earn income, keep expenses low, invest the difference in actual assets (rental property, stocks, business, anything generating cash flow). Accumulate assets that generate income. Reinvest that income into more assets.

Result: Income from job PLUS income from assets, growing passively over time. Eventually asset income exceeds expenses—financial independence. You might not own lots of stuff, but you possess genuine wealth.

The example: Person A earns $80,000/year, spends $78,000 on lifestyle (car payment, big rent, nice things), saves $2,000. Person B earns $60,000/year, spends $40,000 (modest lifestyle), invests $20,000 annually in assets. After ten years, Person A has nicer stuff but no wealth. Person B has modest stuff but $200,000+ in assets generating additional income. Guess who's financially free earlier?

The cultural messaging problem: Advertising and social pressure push liabilities disguised as assets. "Invest in yourself" by buying expensive clothes. "Build wealth" by buying a house you can barely afford. "You deserve it" for the luxury car. All of these are liabilities, but they're marketed as investments or assets.

The keeping-up-with-the-Joneses trap: Everyone around you is buying liabilities (nice cars, big houses, designer goods), so you assume that's what financial success looks like. Meanwhile the actual wealthy people are driving older cars, living in modest homes, and accumulating income-generating assets. But you can't see their assets—you can only see the liabilities.

How to Start Building Real Assets (Practical Steps)

Knowing the difference is useless without action. Here's how to actually shift from accumulating liabilities to building assets.

Step 1: Calculate your current position. List everything you own. For each item, determine if it generates income (asset) or costs money (liability). Be brutally honest. Most people discover they have mostly liabilities with few or zero assets. This is the wake-up call.

Step 2: Stop buying liabilities. Before any purchase, ask: "Is this an asset or liability?" If it's a liability, ask: "Do I genuinely need this, or do I just want it?" Buying liabilities isn't forbidden, but do it consciously and minimize them.

Step 3: Reduce existing liabilities. Pay off car loans, sell vehicles you don't need, downsize housing if it's eating too much income, cancel subscriptions you don't use, sell electronics and goods you don't need. Convert liabilities to cash, even if you take losses. Cash can buy assets; liabilities can't.

Step 4: Build emergency fund first. Before investing in assets, have 3-6 months expenses in savings. This prevents you from having to sell assets in emergencies.

Step 5: Start with accessible assets. For most people, this means index funds or ETFs. Open a brokerage account, invest in broad market index funds, reinvest dividends. Start with whatever you can afford—$100/month is infinitely better than zero.

Step 6: Learn about other asset classes. Real estate requires more capital and knowledge, but rental properties are one of the most reliable wealth-building assets. Businesses require skill and risk but can generate significant returns. Bonds are stable but lower return. Diversification across asset types reduces risk.

Step 7: Reinvest asset income. When assets generate income, don't spend it on liabilities. Reinvest it into more assets. Compound growth is how small asset bases become large ones over decades.

Step 8: Track net worth quarterly. Calculate total assets minus total liabilities. This number should increase over time if you're building wealth. If it's stagnant or declining despite earning income, you're accumulating liabilities faster than assets.

The timeline: This isn't quick. Building meaningful asset bases takes years or decades. But every year you delay is another year of accumulating liabilities instead of assets. Start now, even small.

The Bottom Line

Assets vs liabilities explained through the cash flow lens: Assets put money in your pocket through income generation. Liabilities take money out through ongoing costs.

Most things people think are assets are liabilities: Your car (unless monetized) is a liability. Your primary residence (unless generating income) is functionally a liability. Electronics, furniture, designer goods, boats, subscriptions—all liabilities.

True assets generate income: Rental properties cash flowing after expenses. Dividend stocks. Profitable businesses. Interest-bearing bonds or savings. Royalty-generating intellectual property.

Why this matters: Rich people accumulate assets. Middle-class people accumulate liabilities while thinking they're assets. Poor people have neither (often because all income goes to survival). Understanding the difference determines which category you end up in.

The action steps: Stop accumulating liabilities, reduce existing ones, start buying assets with freed-up cash, reinvest asset income into more assets, repeat for decades.

This isn't glamorous. You won't look wealthy while doing it—you'll look modest while others flash liabilities. But in twenty years, you'll have income-generating assets while they're still working to pay for depreciating stuff.

Your car isn't making you wealthy. Your designer bag isn't building financial security. Your financed furniture isn't an investment.

They're liabilities. Expensive ones.

Now you know. What you do with that knowledge determines your financial future.

Start thinking in cash flow. Start buying assets. Stop pretending liabilities are assets.

Your future self—the one who might actually achieve financial independence—will thank you.

Or you can keep buying nice stuff and staying broke despite good income.

Your choice. But at least now it's an informed choice.

You're welcome.

Now go calculate your actual net worth and probably get depressed.

Then fix it.

Comments

No comment yet. Be the first to comment