50/30/20 Rule vs Zero-Based Budgeting — Which Budgeting Method Actually Works for You

By: compiled from various sources | Published on May 25,2026

Category Intermediate

Description: Discover the 50/30/20 rule vs zero-based budgeting and which method works best for your life. An honest, practical guide to finding the right budgeting approach in 2026.

Every Budgeting System Promises to Fix Your Finances. Here Is the Honest Truth About Which One Actually Will.

Let me tell you about two people I know who tried to fix their finances in the same month.

The first person — Anjali, a marketing professional in Bengaluru earning fifty-two thousand rupees per month — downloaded a budgeting app, read about the 50/30/20 rule, spent thirty minutes setting up her categories, and launched her new financial life with genuine enthusiasm on the first of the month.

By the fifteenth, she had abandoned it. Not because the rule was wrong. Because her rent alone consumed forty-four percent of her income, which meant her numbers did not fit the framework from day one, which made the whole exercise feel broken before it began.

The second person — Rajan, a software developer in Hyderabad earning eighty thousand rupees per month — adopted zero-based budgeting after watching a YouTube video that made it sound transformative. He spent an entire Sunday assigning every rupee of his income to specific categories. He felt organised and in control.

By the third week, he had spent four hours updating his budget spreadsheet to account for a two-hundred-rupee coffee he had not planned for, missed a category, got frustrated with the administrative complexity, and quietly stopped tracking entirely.

Neither system failed them because it was a bad system. Both systems failed them because they were the wrong system for the specific person trying to use them.

This guide is about understanding the genuine difference between the two most popular budgeting approaches — the 50/30/20 rule and zero-based budgeting — what each actually does, who each actually works for, and how to choose the one that fits your real life rather than your ideal life.

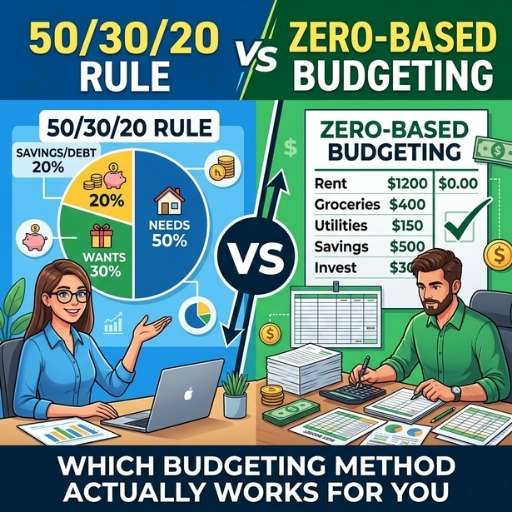

The 50/30/20 Rule — What It Actually Is

The 50/30/20 rule was popularised by US Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their 2005 book All Your Worth. It divides after-tax income into three broad categories.

Fifty percent goes to needs — the non-negotiable expenses without which life functioning is genuinely compromised. Rent or home loan EMI. Utilities. Groceries. Basic transportation. Insurance premiums. Minimum debt payments.

Thirty percent goes to wants — the discretionary spending that makes life enjoyable rather than merely functional. Dining out. Entertainment. Hobbies. Clothing beyond basic need. Travel. Subscriptions chosen for enjoyment.

Twenty percent goes to savings and debt repayment — the forward-looking allocation that builds financial security and eliminates debt. Emergency fund contributions. Investment SIPs. PPF contributions. Additional debt repayment beyond minimums.

That is genuinely the whole system. No subcategories within each bucket. No tracking of individual transactions. Just three percentages applied to monthly income and a general awareness of which bucket each spending decision falls into.

What the 50/30/20 rule is designed to do:

It provides a simple framework that requires minimal ongoing management while ensuring that the most important financial priority — saving and debt repayment — gets a defined allocation before discretionary spending consumes it. The twenty percent savings allocation is the rule's most important feature — it makes saving a predetermined commitment rather than an afterthought.

What the 50/30/20 rule does not do:

It does not help you understand specifically where money is going within each bucket. It does not tell you which specific wants to cut when the wants bucket is overrun. It does not help you optimise spending within categories. And crucially, it does not work for people whose needs genuinely consume more than fifty percent of income — which in high-cost Indian cities is a very large portion of the population.

Zero-Based Budgeting — What It Actually Is

Zero-based budgeting operates on a fundamentally different principle. Every rupee of monthly income is assigned to a specific category before the month begins until the total assigned equals the total income. Income minus all assigned categories equals zero — hence the name.

The process works like this. You start with your total monthly income. You list every category of spending and saving you anticipate for the coming month — rent, groceries, electricity, phone bill, dining out, entertainment, fuel, SIP investment, emergency fund, clothing, and every other category relevant to your life. You assign a specific rupee amount to each category. You add all the assigned amounts. The total must equal your total income. If there is money left unassigned, it gets assigned — to savings, to debt repayment, or to a specific category that deserves more. If the total exceeds income, categories get reduced until the budget balances.

Then throughout the month you track every actual expense against its assigned category. When a category runs out, the spending in that category stops — or you consciously move money from another category to cover it, accepting the explicit trade-off that involves.

What zero-based budgeting is designed to do:

It creates complete intentionality about every rupee — nothing happens by default, everything is chosen. It eliminates category-level overspending by making the limit explicit before spending begins. It reveals exactly where money is going at a granular level. And it forces a confrontation with financial priorities by requiring every allocation to be actively decided rather than passively allowed.

What zero-based budgeting does not do:

It does not run itself. It requires significant ongoing attention — tracking transactions, updating categories, reconciling reality against the plan. It is not forgiving of the kind of life complexity that produces unplanned expenses regularly. And it demands a relationship with financial administration that some people find genuinely sustaining and others find genuinely exhausting.

The Honest Comparison — Side by Side

| Dimension | 50/30/20 Rule | Zero-Based Budgeting |

|---|---|---|

| Setup time | 30 minutes initially | 2 to 4 hours initially |

| Ongoing maintenance | Minimal — monthly check | Significant — ongoing tracking |

| Specificity of insight | Low — broad category awareness | High — transaction-level detail |

| Flexibility | High — buckets absorb variation | Low — requires explicit category adjustment |

| Forgiveness of complexity | Very forgiving | Demanding |

| Works for variable income | Reasonably well | Challenging without adaptation |

| Best financial outcome potential | Moderate — ensures savings happen | High — if maintained consistently |

| Most common failure mode | Needs exceed 50% making framework feel broken | Administrative burden causing abandonment |

| Requires financial enthusiasm | No — works for reluctant budgeters | Yes — rewards engaged budgeters |

Who the 50/30/20 Rule Actually Works For

The person who needs a system that runs mostly on autopilot.

The 50/30/20 rule's greatest strength is its minimal ongoing management requirement. Once you have set up automatic transfers for the twenty percent savings allocation and have a general sense of your needs versus wants categories, the system requires perhaps thirty minutes of monthly review rather than ongoing daily attention.

For people with demanding jobs, demanding family situations, or simply a limited appetite for financial administration — which is most people — this low-friction design is the difference between a system they maintain and a system they abandon.

If your honest self-assessment is that you will not consistently track every transaction, the 50/30/20 rule gives you the most important thing — a protected savings allocation — without requiring the ongoing engagement you are unlikely to sustain.

The person at an early stage of financial organisation.

If you have never budgeted before, have no emergency fund, and are broadly aware that your spending is uncontrolled without understanding the specifics — the 50/30/20 rule is an excellent starting point. It provides immediate structure without requiring you to understand your spending patterns in detail before you can begin.

The twenty percent savings commitment, implemented through automatic transfer on salary day, is the most valuable feature. Everything else can be improved over time as financial habits develop.

The person with a stable, predictable income and spending.

The 50/30/20 rule works most naturally when income and major expenses are stable and predictable — the same salary each month, the same rent, the same EMIs. In this context, the three buckets fill predictably and the main task is managing the wants bucket sensibly.

For salaried employees with relatively stable lifestyles, the 50/30/20 rule often works well enough to produce meaningful financial progress without requiring more complexity.

Who Zero-Based Budgeting Actually Works For

The person who genuinely wants to understand where every rupee goes.

Zero-based budgeting rewards financial curiosity and engagement. If you find yourself genuinely interested in understanding your spending patterns, in optimising every category, and in the satisfaction of a precisely balanced budget — zero-based budgeting provides that engagement in a way the 50/30/20 rule cannot.

The people who maintain zero-based budgets successfully long-term almost universally describe it as satisfying rather than burdensome — which reveals an important truth about the system. It works best for people whose temperament finds detailed financial tracking engaging rather than draining.

The person whose spending has specific problem areas they need to address.

If you know you have a specific spending problem — food delivery is consuming an extraordinary amount, subscriptions have accumulated beyond any reasonable review, clothing spending is significantly higher than you want it to be — zero-based budgeting's category-level specificity is the tool that actually reveals and addresses it.

The 50/30/20 rule might tell you that your wants bucket is overrun at forty percent of income rather than thirty. It does not tell you specifically that food delivery alone is consuming eight thousand rupees per month. Zero-based budgeting tells you exactly that — and makes the specific reduction decision concrete and visible.

The person trying to aggressively accelerate debt repayment or savings.

When the financial goal is maximum acceleration — paying off a significant debt as fast as possible, saving for a specific large goal within a specific timeframe — zero-based budgeting's precision is genuinely more powerful than the 50/30/20 rule's broad strokes.

Assigning specific rupee amounts to every category forces the confrontation with trade-offs that acceleration requires. Do you reduce the dining out category by three thousand rupees per month to pay down the personal loan two months faster? Zero-based budgeting makes that trade-off explicit and visible. The 50/30/20 rule keeps it vague.

The person with irregular or variable income.

This one is counterintuitive because zero-based budgeting seems like it would be harder with variable income — and it is more complex to implement. But done correctly, zero-based budgeting on variable income — building the budget each month based on actual expected income for that month rather than an average — actually handles income variability better than the 50/30/20 rule.

When income is lower than average, zero-based budgeting forces explicit priority decisions about which categories get reduced. The 50/30/20 rule applied to variable income often results in unconscious overspending in low-income months because the percentages feel fixed rather than flexible.

Freelancers, consultants, commission-based earners, and anyone with genuinely variable monthly income who uses zero-based budgeting — building a conservative budget from their minimum expected income and allocating windfalls explicitly — often find it more honest to their actual financial situation than percentage-based systems.

The Indian Context — Why Both Systems Need Adaptation

Both the 50/30/20 rule and zero-based budgeting were developed primarily in Western economic contexts and require honest adaptation for Indian financial realities.

The rent problem with the 50/30/20 rule in Indian cities.

In Mumbai, Bengaluru, Delhi, and other major Indian metros, rent alone frequently consumes thirty-five to fifty percent of middle-income salaries — sometimes more. Adding other genuine needs — groceries, utilities, transportation, insurance — pushes the needs category well past fifty percent for a very large portion of the urban Indian population.

When needs consume sixty or sixty-five percent of income, the 50/30/20 rule's fifty percent target creates immediate failure without any actual financial mismanagement. The framework needs explicit adaptation.

The most honest adaptation is calculating your actual needs percentage and then dividing the remaining income between wants and savings in the 30-20 proportion — or more aggressively toward savings if the financial situation is tight. A sixty-ten-thirty split for someone whose needs genuinely consume sixty percent is not failure. It is honest calibration.

The joint family and obligation context.

Many Indian households include financial obligations — to parents, to siblings, to extended family — that Western budgeting frameworks do not account for. Regular transfers to parents in another city, contributions to siblings' education, participation in family financial events — these are genuine financial realities that need explicit category treatment in any honest Indian budgeting system.

Zero-based budgeting handles this better than the 50/30/20 rule because it allows explicit category creation for family obligations — they get an assigned amount like any other spending category, which removes the guilt and confusion of treating them as either needs or wants.

The cash and UPI transaction challenge.

Much of India's spending still happens through cash and UPI in ways that are harder to automatically categorise than credit card spending. Zero-based budgeting's transaction-level tracking is more demanding in a predominantly UPI and cash economy because many transactions require manual entry rather than automatic import.

The practical response is using UPI consistently from a primary account that can be reviewed monthly, maintaining the habit of capturing significant cash spending in real time through a simple note-taking approach, and accepting that some cash spending will be approximated rather than precisely captured.

A Third Option — The Hybrid Approach

Here is something that most budgeting advice does not acknowledge but that many successful personal finance practitioners actually use.

The 50/30/20 rule and zero-based budgeting are not mutually exclusive. A hybrid approach uses the 50/30/20 rule's broad structure for overall allocation while applying zero-based budgeting's specificity to the one or two categories that most need granular management.

How the hybrid works in practice:

Implement the 50/30/20 rule's most critical feature — the automatic savings transfer — without managing the full framework. Know your needs percentage honestly and ensure it is sustainable. Apply zero-based budgeting specifically to the wants category — the one most likely to overspend — by assigning specific amounts to specific want subcategories at the start of each month.

This approach provides the savings protection of the 50/30/20 rule with the specific spending control of zero-based budgeting in the area where control matters most — without requiring the full administrative burden of complete zero-based tracking.

For most people most of the time, this hybrid produces better outcomes than either pure system — because it matches the right level of specificity to the right categories based on where the actual financial challenges live.

How to Choose — The Honest Self-Assessment

Rather than recommending one system universally, here is the honest self-assessment that reveals which approach fits your specific situation.

Choose the 50/30/20 rule if:

You have never successfully maintained a budget for more than two months. You find detailed financial tracking genuinely draining rather than engaging. Your income is stable and your spending is relatively predictable. You primarily need to ensure savings happen consistently rather than understand spending precisely. You prefer a system that runs mostly in the background to one that requires regular active management.

Choose zero-based budgeting if:

You have tried the 50/30/20 rule or similar simple approaches and found that the wants bucket keeps overrunning without understanding why. You have specific spending categories you know are problematic but cannot quantify precisely. You are working toward an aggressive financial goal — debt elimination, specific savings target — that requires maximum allocation optimisation. You genuinely find financial tracking engaging or are willing to build that engagement as a skill. Your income is variable and requires honest monthly recalibration.

Choose the hybrid if:

You want the simplicity of the 50/30/20 rule overall but know that one or two specific spending categories need granular management. You have attempted both systems and found pure versions of each unsustainable for different reasons. You want to start simple and add complexity as your financial habits develop.

The Implementation — Starting This Month

Whichever system you choose, implementation begins with two things that both systems share.

First — automate the savings before anything else. Whether you use 50/30/20 or zero-based budgeting, the savings allocation must become automatic — a transfer that happens on salary day before discretionary spending begins. This is the single most important feature of any budgeting system and the one that produces the most financial impact regardless of which framework surrounds it.

Second — start with honest numbers rather than aspirational ones. The most common implementation failure is building a budget based on what you wish you spent rather than what you actually spend. Pull three months of actual transaction data before setting any category limits. Build the budget around what is true, then adjust toward what you want to be true incrementally.

Final Thoughts — The Best Budget Is the One You Actually Use

Here is the honest conclusion that all the comparison and analysis leads to.

The 50/30/20 rule is not objectively better than zero-based budgeting. Zero-based budgeting is not objectively better than the 50/30/20 rule. The best budgeting system is the one that fits your specific temperament, your specific financial situation, and your specific life complexity well enough that you actually maintain it across the months and years that financial progress requires.

A perfect zero-based budget maintained for three months then abandoned produces worse outcomes than an imperfect 50/30/20 system maintained consistently for three years. A simple savings automation with no formal budget at all produces better outcomes than any sophisticated system that exists only in a spreadsheet that stopped being updated in month two.

The system serves the goal. The goal is financial progress — savings accumulating, debt reducing, financial security building — over time. Choose the system most likely to produce that outcome given who you actually are rather than who you wish you were when it comes to financial management.

Then start. This month. With whatever income arrives this cycle.

Because the best time to begin was last year. The second best time is now.

Frequently Asked Questions (FAQs)

Q1. Which budgeting method is better for beginners — 50/30/20 or zero-based? The 50/30/20 rule is almost always better for genuine beginners. Its simplicity — three categories, minimal tracking, automatic savings as the primary mechanism — makes it possible to implement immediately without requiring detailed knowledge of your current spending patterns. Zero-based budgeting requires building a complete category list before you can start, which requires data that beginners typically do not have. The 50/30/20 rule gets the most important thing — automatic savings — in place quickly, allowing financial habits to develop before adding the complexity of granular category tracking.

Q2. Can the 50/30/20 rule work if rent takes more than 50% of income? Yes, with explicit adaptation. If genuine needs including rent consume sixty percent of income, adapt the framework to a sixty-ten-thirty split — sixty percent needs, ten percent wants, thirty percent savings — or whatever honest proportion reflects your actual situation. The critical feature to protect is the savings percentage. Reducing wants to accommodate high housing costs while protecting savings is the right adaptation. Treating the framework as broken because the needs percentage exceeds fifty and abandoning the savings commitment is the wrong response.

Q3. How long does it take to see results from zero-based budgeting? Most people who maintain zero-based budgeting consistently report meaningful spending insight within the first month and meaningful financial improvement within three months. The first month is primarily data collection — you discover where money actually goes, which is often significantly different from where you believed it went. The second and third months involve category adjustment based on that data. By month three, the budget reflects genuine spending patterns adjusted toward financial goals, and the compounding benefit of controlled spending begins to produce visible savings accumulation.

Q4. Is zero-based budgeting practical for Indian households with cash spending? It requires adaptation but is practical. The key adjustments are using UPI consistently from a single reviewable account for as much spending as possible, maintaining a simple daily note of significant cash expenses, categorising ATM withdrawals as a general cash category with estimated subcategory breakdown rather than precise tracking, and accepting that some approximation is better than abandoning the system entirely. Perfect zero-based tracking is rarely achievable in a mixed cash and digital spending environment — practical zero-based budgeting with good approximation for cash components is both achievable and effective.

Q5. Can I switch from one system to the other if it is not working? Absolutely, and doing so is a sign of financial intelligence rather than failure. The most important thing is maintaining the savings automation regardless of which system framework surrounds it. If you switch from zero-based budgeting to the 50/30/20 rule because the administrative burden became unsustainable, keep the automatic savings transfer in place and adjust the system around it. If you switch from the 50/30/20 rule to zero-based budgeting because you need more spending visibility, maintain or increase the savings commitment while adding category-level specificity. The system is the vehicle — the savings habit is the destination.

Comments

No comment yet. Be the first to comment